Recommended

Event

Designing the New UN Climate Finance Goal

HYBRID

June 04, 2024 10:30—12:00 PM EST | 3.30-5 PM BST | 4.30-6 PM CEST

Developed countries committed to provide or mobilise $100 billion (bn) per year in climate finance by 2020. Although that goal was missed, the OECD suggested last year that it was likely that the goal had been met in 2022. In this note, we use newly available bilateral and multilateral finance data to provide an estimate of climate finance in 2022 based on the OECD’s approach and interpretation of the target. After the introduction, we look at these two sources of finance in turn, before concluding on the overall volumes, and how progress has been made.

The $100bn target, progress, and plans

At COP15 in 2009, countries agreed on a climate finance target—for developed countries to jointly mobilise $100bn per year by 2020 to address the needs of developing countries. Although many were under the impression this finance would be “new and additional” to existing development finance flows, as stipulated in the 2009 Copenhagen Agreement, the OECD and UN have only measured the total amounts of climate finance provided, without considering existing levels of climate or development finance. Even on this basis, according to the OECD, total climate finance had only reached $83bn in 2020.

At COP26, the developed countries laid out a Climate Finance Delivery Plan (CFDP) which made two forward-looking projections from 2021–2025, each envisioning the target would be met in 2023. The OECD’s most recent assessment reported that $89.6bn of climate finance was provided in 2021 and that “preliminary and as yet unverified data” suggested countries may have met the target $100bn in 2022.

In this analysis, we use newly published bilateral data from the OECD’s creditor reporting system along with multilateral finance data to estimate climate finance for 2022.[1] We measure the total finance to “developing countries” that is attributable to “developed countries”.[2] We set these calculations out in turn below.

Multilateral finance for climate

Finance provided through multilateral channels—from the multilateral development banks (MDBs) and multilateral climate funds—has historically been the largest contributor towards the climate finance goal, providing $38.7bn (43 percent) of the nearly $90bn total in 2021.

To calculate its estimate, the OECD uses activity-level data on core budget outflows. Though these are not publicly available, the MDBs also release a comprehensive joint report on climate finance annually, the latest of which includes data for 2022 and which we use here. In line with the OECD, we only include finance attributable to developed countries and received by developing countries. To isolate finance attributable to developed countries, we apply coefficients provided by the OECD based on their shareholding in each institution (in aggregate, developed countries are responsible for 75 percent of total MDB finance). The MDBs also report MDB-managed external resources, including earmarked (multi-bi) and multilateral climate fund finance. We exclude this finance and add finance from the eight multilateral climate funds included by the OECD to avoid double-counting.[3]

Our estimate of multilateral climate finance using data from the MDB joint reports and the multilateral climate funds produces a close match with the OECD’s assessment (averaging within 5 percent); our estimate for 2021 is within $300m (or 0.7 percent) of the OECD assessment. It seems likely that the largest deviation, in 2020, is partly attributable to the COVID pandemic, but other factors such as imperfect assumptions about the proportion of regionally allocated funds going to developing countries also impact the accuracy. Over the seven years we analyse, our estimates produce a lower figure in five of the years with only 2015 and 2016 fractionally higher. On this basis, the OECD assessment is likely to be higher than ours. We estimate that, in 2022, multilaterals provided $46.2bn of climate finance relevant to the $100bn target (of which $44.2bn was from the MDBs and $2bn from the multilateral climate funds), an increase of $7.5bn since 2021.

The significant—almost threefold—increase in the volume of climate finance provided by MDBs since 2015 is a result of both a higher volume of finance overall and an increase in the share of finance with climate objectives. In 2015, about 15 percent of the MDBs’ total operations of $130bn was climate finance for developing countries.[4] That proportion has increased (with a drop in 2020, probably due to covid), and of the total $250bn of finance provided in 2022, 24 percent was climate finance.[5]

Figure 1. Multilateral (L) and bilateral (R) climate finance—CGD estimate and OECD outturn ($ billions)

Note: Dotted lines show CGD climate finance estimates for 2022.

Source: Authors’ analysis of OECD climate finance tracking and (L) MDB Joint Reports on Climate Finance and (R) OECD Creditor Reporting System.

Bilateral finance

Official reporting to the United Nations Framework Convention on Climate Change (UNFCCC) of bilateral climate finance is only undertaken every two years, though a majority is reported sooner to the OECD’s Creditor Reporting System (CRS) as either official development assistance (ODA) or other official flows (OOFs). The CRS was updated in December 2023 with detailed data for 2022, and we use this to approximate bilateral climate finance provision by developed countries.

CRS data are tagged with a Rio Marker which denotes if climate is a “principal” or “significant” objective of the finance. Countries apply a coefficient to the value of the finance to calculate the climate element—most using fixed coefficients for each marker, and others on a case-by-case basis. Most countries use principal coefficients of 100 percent and significant coefficients between 30 and 50 percent, though these are highly variable between providers. We use fixed coefficients where they are provided (in reporting to the UNFCCC) and a coefficient of 100 percent for principal and 42 percent for significant where these are unknown.[6] The face value of climate-tagged finance in the CRS was worth $48.2bn in 2022. Adjusting this value using the Rio Marker coefficients results in a value of $33.8bn, an increase from $24.4bn in 2021.

While ODA is comprehensively reported to the CRS, many climate finance flows that count as OOFs are not; over the past decade, based on our estimates some 31 percent of total bilateral climate finance was not reported to the CRS (the right-hand chart above shows this as the difference between the OECD and CRS lines). As such, we add an estimate of these flows based on historical levels. In our central estimate, we assume these are the average of $10.4bn seen since 2015 (excluding 2020 which appears unusually low, likely due to COVID).

We add the estimated $10.4bn of unreported OOFs to our figure of $33.8bn to estimate that bilateral climate finance was $44.2bn in 2022, $9.7bn higher than the 2021 value of $34.5bn. Our more conservative estimate—that unreported OOFs are at $8.6bn, their lowest level since 2015 (again excluding 2020)—would result in bilateral climate finance of $42.4bn, still the largest single-year increase in bilateral climate finance since the OECD began tracking.

This $9.7bn increase in climate finance accounts for almost all of the increase in total reported bilateral assistance (excluding the costs of hosting refugees within donor countries) which rose by $10.3bn to $154.2bn in 2022, with climate’s share rising from 17 to 22 percent. The increase in bilateral climate finance appears therefore to be on top of existing finance. However, if support to Ukraine is excluded from the analysis ($18.8bn in 2022, up from $1.8bn in 2021) then it is clear the latest increase in climate spend was achieved by refocusing or rebadging existing development assistance; with its share rising to 25 per cent.[7]

Over the longer-term, we can see bilateral climate finance increased by 71 percent since 2015 reflecting both an increase in overall bilateral assistance (by 42 percent excluding refugee funding) and an increased share focussed on climate from 16 percent in 2015 to 22 percent in our 2022 estimates.

So, where does this leave progress on the $100bn goal?

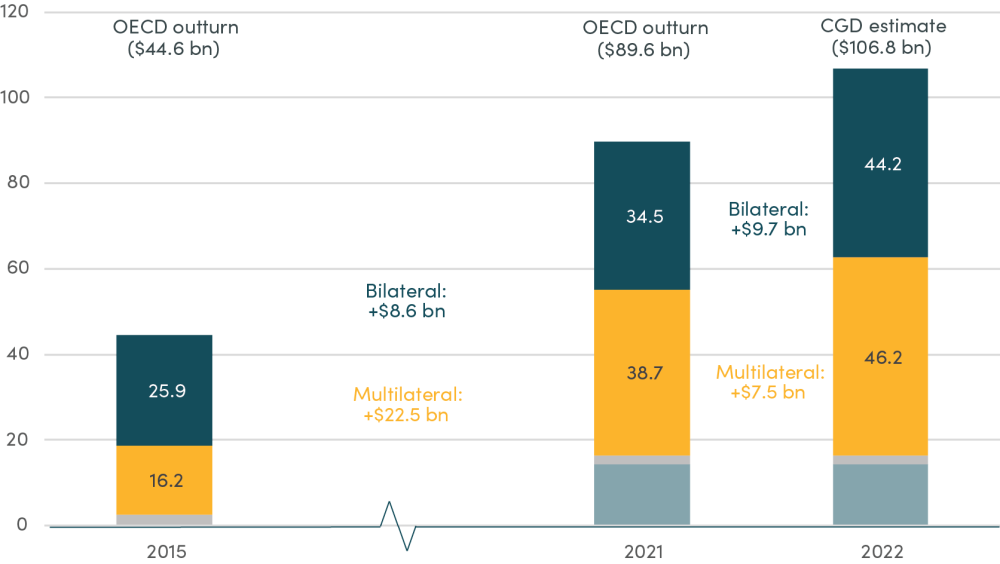

Our analysis suggests with a high degree of confidence that the $100bn goal was met in 2022 using the OECD’s definition of the target. We do not make estimates of the contributions from mobilized private finance or export credits, assuming instead—conservatively—that these are unchanged from 2021 at $14.4bn and $2bn respectively. Combined with our estimates for multilateral ($46.5bn) and bilateral ($44.2bn) public finance, this suggests that we might expect 2022 climate finance to total $106.8bn. This would mark an increase on the 2021 figure of $17.2bn—the largest single-year increase since the OECD began tracking in 2013. Our assumptions err on the conservative side, and the final figure may be higher; even using our more conservative estimates of multilateral ($44.9bn) and bilateral ($42.4bn) public finance, we estimate the $100bn target was exceeded in 2022 by more than $3.5bn.

As the target of $100bn runs from 2020 through to 2025, there is an argument that shortfalls in previous years should be made up. Any amount above $100bn would contribute to those arrears from 2020 ($16.7bn) and 2021 ($10.4bn), and our calculations suggest the total shortfall would be down to just over $20bn as of 2022.

Across both bilateral and multilateral providers, the target was partly achieved by adding climate objectives to existing development finance flows. This was particularly visible in 2022 where total bilateral finance (excluding Ukraine and refugee-hosting) fell, but our estimates suggest bilateral climate finance rose with 5 percent refocussed on climate in a single year.

The overall picture of combined climate and development finance makes clear that donors’ financial effort—expressed as a share of their combined economies (GNI)—has actually fallen since 2009. We calculate that relevant bilateral, multilateral and export finance was 0.44 percent of providers’ GNI in 2022 relative to 0.45 percent in 2009.[8] In face value terms, this was an increase of $67.2bn in total finance. This suggests that 63 percent of climate finance was additional in terms of the face value, with 37 percent coming from existing flows.[9]

Figure 2. Total climate finance—OECD outturn and CGD estimate ($ billions)

Source: Authors analysis and OECD climate finance tracking. Grey bars show private mobilised finance ($14.4bn, unavailable in 2015) and export credits and guarantees ($2bn).

In summary, we estimate over $100bn of climate finance was provided and mobilised in 2022. The overall climate and development finance envelope (excluding refugee costs) increased by just under two thirds of this amount since 2009, and as such over a third came from refocussing or rebadging existing finance. If “new and additional” is judged against the nominal or real value of finance provided in 2009, less than two thirds of climate finance could be considered new and additional. Still, judged as a share of provider economies, total development finance fell slightly as a share of GNI from 0.45 to 0.44 percent, suggesting no “new and additional” financial effort.

In November this year, countries will meet at COP 29 to agree a new collective quantified goal (NCQG) for climate finance, a successor to the $100bn per year target. This analysis shows that the design of the current target has encouraged developed country providers to allocate increases in their development finance envelope to climate alongside shifting some existing development finance into climate objectives but with no additional fiscal effort relative to the size of their economies. Given the scale of the challenges of climate and development, we think a new target should prioritize increasing overall resources for climate and development, rather than moving them between objectives.

[1] In 2021, OECD data shows multilateral (43% of the total) and bilateral (39%) public finance contributed the great majority of climate finance with private finance mobilised (16%) and export credits (2%) making up the remainder.

[2] The OECD’s definition of “developed countries” includes all of the UNFCCC’s Annex II parties as well as other EU member states Liechtenstein and Monaco. For “developing countries”, the OECD includes four ODA-eligible recipient countries in addition to the 141 non-Annex I countries from the UNFCCC. We used the OECD classifications, full breakdown here.

[3] As per the OECD’s provided coefficients, these are the: Adaptation Fund; Climate Investment Funds; Global Environment Facility’s Trust Funds, Least Developed Country Fund, and Special Climate Change Fund; Green Climate Fund, International Fund for Agricultural Development; and the Nordic Development Fund.

[4] Of MDBs included in the MDB joint reports on climate finance. Islamic Development Bank was first included in 2019, the Asian Infrastructure Investment Bank in 2020, and the Council of Europe Development Bank and New Development Bank in 2022.

[5] In some MDBs, the increase has been even more significant. In 2015, the African Development Bank provided $1.2bn of its $8.3bn operations as climate finance — or 15%; in 2022, it provided $3.6bn of its (unchanged) total operations — 45%.

[6] The 42% coefficient for the significant marker is calculated as an unweighted average of known fixed coefficients, excluding the 100% coefficients of Czech Republic, Iceland, Poland, and Slovenia.

[7] Around 2% ($389m) of aid going to Ukraine in 2022 is tagged with a climate marker. Negligible volumes of IDRC are tagged with a climate marker. If the substantial £18.8bn support to Ukraine is excluded, remaining countries saw development finance fall $7.3bn to $135.4bn.

[8] Excluding in-donor refugee spend which is recordable as “development assistance” but is not a form of development finance.

[9] We have also looked at the increase in constant prices. Remarkably, this shows an increase ($67.3bn in OECD’s 2021 constant prices) which is very similar to that in current prices (against a total climate finance figure $102.0bn in constant 2021 terms). This appears to be explained by the rising value of the dollar over the period offsetting the effect of inflation. These figures imply that the real terms increase in overall development finance meant that 66% of climate finance was additional in real terms, while the remaining 34% was refocussed or rebadged from existing development finance.

Topics

CITATION

Mitchell, Ian, and Edward Wickstead. 2024. Has the $100 Billion Climate Goal Been Reached? . Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Wanan / Adobe Stock