Recommended

BRIEF

Maximising the Impact of EU Climate Finance

Blog Post

The EU’s Carbon Border Tax

Summary

- The EU’s Carbon Border Adjustment Mechanism (CBAM) incentivises key countries, including China and India, to assess their policies around industrial carbon emissions.

- But CBAM faced criticism from low-income countries at COP28, with evidence suggesting that its economic impact on Africa could be as much as three times the amount of EU aid to the continent.

- While major emerging economies should face the full incentives from CBAM, lower income countries require a different approach.

- The Commission must review CBAM's impact on least developed countries (LDCs) by 2025. We propose it collaborates with the Council and Parliament to reform CBAM in two ways:

- Implement a longer transition period for LDCs, following the principle of "Common but Differentiated Responsibilities"

- Revisit the European Parliament’s proposal to allocate additional finance to the most vulnerable countries, by proposing that CBAM revenues be used to finance climate-related loss and damage, amounting to around 1 percent of the Commission’s annual budget by 2030.

- These reforms would show the EU is listening to partner countries and provide a new and additional source of climate funding. This would transform its reputation and strengthen its international negotiating position.

What are the issues?

EU climate ambitions

The EU has set ambitious climate goals, both domestically and internationally. The European Emissions Trading Scheme (ETS) has been a cornerstone of EU climate policy since 2005, through the introduction of market-based incentives for polluters within the bloc to decrease their emissions. The EU Green Deal, launched in 2020, the adoption of the EU Climate Law, and the Fit for 55 package have further underlined these domestic ambitions. The EU has also increasingly been externalising major aspects of these policies—most notably through the introduction of the Carbon Border Adjustment Mechanism (CBAM), which aims to prevent carbon “leakage” by linking charges for imports with carbon prices set by its ETS, and pushes major emitters like China and India to consider domestic carbon pricing.

The EU’s Carbon Border Adjustment Mechanism (CBAM) is a critical tool, both for gaining the support of domestic voters and stakeholders for carbon pricing; and in incentivizing other major economies—including the US, China, and India—to accelerate their plans to tackle carbon in industry. Already, there are signs that Chinese and Indian industries are considering how to respond to these proposals seriously, some other countries—including Australia, Türkiye, and the UK—are now considering developing their own carbon border levies.

However, CBAM does not currently take account of the different levels of development or emissions in partner countries, nor their ability to decarbonize relevant industries. This has led to significant criticism, including at last year’s COP, and the legislation faces potential legal obstacles within the World Trade Organization. [1] It applies equally to the US and Australia—whose populations emit around 15 tonnes of CO2 per person every year, as to Mozambique, whose average citizen accounts for just 0.2 tonnes of CO2 every year.[2]

Box 1. What is CBAM?

The Carbon Border Adjustment Mechanism, CBAM, is the EU's tool to put a price on the carbon emitted during the production of carbon intensive goods that are entering the EU. This aims to level the playing field with EU producers, many of whom already pay a carbon price, and to encourage cleaner industrial production in non-EU countries. It will initially apply to imports of cement, iron and steel, aluminium, fertilisers, electricity and hydrogen.

From 2026, the EU will require that importers declare emissions embedded in their imports; and purchase certificates for any emissions based on the cost paid by EU producers. If imports can prove products have already paid a carbon price in their country, this amount can be deducted from the charge.

CBAM is currently in a transitional phase (2023-25) where importers are required to report greenhouse gas emissions (GHG) embedded in their imports (direct and indirect emissions), without the need to buy and surrender certificates.

What is CBAM’s impact in poorest countries?

The most likely scenario estimated by the African Climate Foundation and LSE showed that ,once fully implemented, CBAM could reduce African GDP by nearly 1 percent, equivalent to USD 25 billion (EUR 23 billion), which is roughly three times the USD 6.5 billion (EUR 6.2 billion) provided in total Official Development Assistance to the continent by the European Commission and European Investment Bank (EIB). This reflects the importance of trade with the EU for African economies. These countries have made virtually no contribution to the climate change problem, but are being asked to pay a significant price to those who have. [3] Even now, sub-Saharan Africa’s emissions are under a tonne per head, relative to over 5 tonnes in the EU.

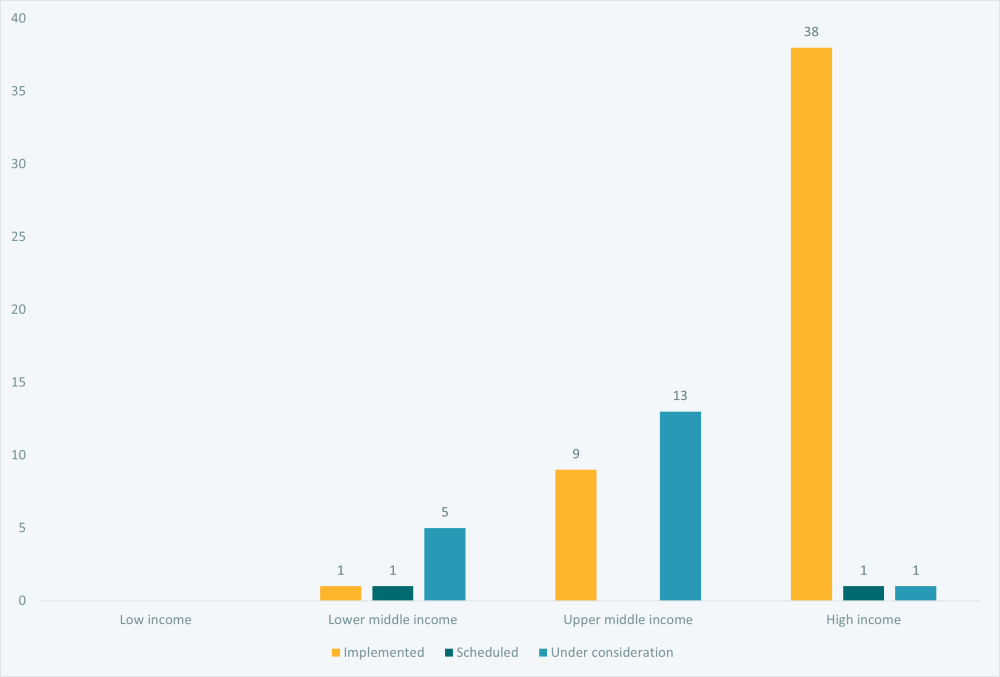

In principle, these countries could avoid paying CBAM by implementing their own domestic carbon price. While doing so could have in the long-term, many of these countries also have relatively weak government capacities to swiftly implement new carbon pricing systems. Our analysis (see Figure 1, below) has shown that only one of 80 low- and lower-middle-income countries have currently implemented a carbon price, and only five have one under consideration. With the current transition phase concluding at the end of 2025; it is clear that many of the 80 poorest countries in the world will be unprepared.

Figure 1. Lower income countries are unprepared for the EU’s CBAM

Source: CGD analysis of World Bank carbon price dashboard, accessed November 2023.

Notes: In the 2022 data, there were 26 LICs, 54 LMICS, 54 UMICs, and 83 HICs. Only regional and national schemes are included in the analysis. The EU’s ETS covers 30 countries (27 EU Member States plus Iceland, Liechtenstein and Norway) and these are included in the HIC bar. Countries are counted only once.

Impact on the EU’s reputation and influence

CBAM has widely been perceived as a protectionist measure, including by the African negotiating group and Brazil; and was arguably a major political own-goal at last year’s COP. The EU’s significant achievements and leadership on climate policy were largely overlooked because CBAM failed to be designed according to the principle of ‘Common but Differentiated Responsibilities’.

Previously, the EU Parliament had proposed the impact of CBAM should lead to a separate increase in finance to LDCs; but the European Council chose not to reallocate any funding from CBAM revenues to partner countries nor increase funding to LDCs.

A related limitation in the EU’s international approach relates to its contribution to the Loss and Damage fund. That fund was launched at COP27 to provide financial assistance to nations most vulnerable and impacted by the effects of climate change. While the EU was one of the first to announce a contribution of EUR 25 million ($27.1 million), because its finances until 2028 are already set as part of its seven-year budget-cycle under the Multiannual Financial Framework (MFF), it was clear this would not represent additional funding, and instead was a simple reallocation of existing development finance. The announcement was therefore undermined by the EU’s inability to provide additional finance and CBAM revenues would be a powerful way to demonstrate the EU’s support for new sources of finance to counter the effects of climate change.

Putting CBAM revenues in context

The Commission should balance the scale of finance expected to be generated by CBAM against the reputational benefit of sharing that revenue with LDCs. Estimates suggest that the European Institutions’ share [4] of annual revenue from the CBAM will be around EUR 1.5 billion in 2028, rising to EUR 2.1 billion by 2030.[5] CBAM revenues would contribute less than 1 per cent towards the EU’s total expected revenue package in 2028 ( (expected to reach at least EUR 180 billion).[6] These revenues have been identified as a contribution towards the repayments of Next Generation EU loans, but would likewise only contribute marginally to these repayments, which are expected to peak at around EUR 27 billion annually in 2030.[7]

Figure 2. CBAM revenues are small relative to the EU budget but significant for poorer countries

Projected scale of CBAM revenues in context of the EU budget and impacts on Africa, (EUR, billions)

Sources: Projected losses of Africa’s GDP due to CBAM converted from USD to EUR using World Bank exchange rates), CBAM revenues until 2030; ETS revenues until 2030; NGEU repayments; current EU budget

Revenues for the CBAM could rise into the next decade, but a strong case would remain for reallocating at least a portion to least-developed and climate-vulnerable countries, reflecting those countries almost negligible contribution to climate change to date. LDCs currently receive some EUR 3.5 billion in ODA from EU institutions, so CBAM revenues could be a material uplift.

In order to rebuild its reputation as a climate leader, the EU should revise its approach to CBAM. As the EU prepares for its next, post-2028 Multiannual Financial Framework (MFF) - the EU’s approach to CBAM must evolve to gain the buy-in of developing countries.

Why should the EU address it now?

At the last COP, criticism of the EU’s CBAM dominated many discussions on EU climate policy. At COP29 this year; there will be discussion of a New Collective Quantified Goal on climate finance before all countries submit new emissions reductions plans (Nationally Determined Contributions) by February 2025. The Commission will likely be unable to commit any new funding to motivate ambitions given the budget cycle and pressures but, alongside tackling the quality of its climate finance outlined in our recent paper, [8] it should signal that it has understood the feedback on CBAM, and respond with plans to review the impact on the poorest countries, and signal its willingness to create a transition period and a mechanism to recycle some of the revenues.

By providing concrete steps to tackle the concerns of the poorest 80 or so developing countries; the EU will empower them to challenge the major emerging economies who are major emitters but identify themselves with the wider developing country group.

What can the EU do about it?

CBAM is a critical step in incentivizing the global transition to net zero, but its economic impact in the poorest countries, especially in Africa, is undermining the EU’s reputation. The Commission is committed [9] to report to the Parliament and the Council on the impact of CBAM on LDCs before the end of the transition period, and this is an opportunity to respond to developing country concerns. The political guidelines for the European Commission for 2024-2029 by Ursula Von der Leyen provide a clear mandate [10]:

“We also need to listen and respond better to the concerns of our partners impacted by European legislation, in particular those linked to the European Green Deal. We need a more systematic approach to assessing the impact of our laws on non-EU countries, and we need to provide more targeted support to help them adjust to and benefit from those laws.”

Given the relatively small scale of revenues expected to be generated by CBAM as compared to its political significance and economic effects on Africa, we propose the Commission works with the Council and Parliament to reform CBAM in two ways.

First, we propose that the new Commission work with the Council and Parliament to design a longer transition period for Least Developed Countries to adjust to the Carbon Border Adjustment Mechanism.

The Commission should implement a longer transition period of an additional five years for LDCs in line with the principle of ‘Common but Differentiated Responsibilities’, which applies across both international trade and climate policy. This would maintain incentives for governments and industry to implement a carbon price and invest to lower carbon; but would provide a more realistic time-frame for adjustment.

Second, we encourage the Commission to work together with the Parliament and Council to commit to redirect some or all of the future CBAM revenues to visibly and credibly scale up new and additional resources for climate finance, including for Loss and Damage.

At least until 2030, this would have minimal fiscal cost for the EU, amounting to just under 1% of the Commission’s current annual budget; but it would be transformational for the EU’s reputation in terms of demonstrating a new source of funds for climate. If the funding was allocated to Loss and Damage, this would be a demonstrable new source of finance, responding to calls for this finance to be distinct and additional to existing climate and development finance. The EU’s regulation on CBAM did not agree text on how the revenues would be used beyond three quarters of revenue flowing to the EU budget. While there is a clear imperative to use this finance towards the borrowing for the COVID recovery plan, the Commission can make the geo-political case to the Council and Parliament to propose that the finance—which falls under the next Multi-Annual Financing Framework period—be allocated to LDCs to deal with the effects of climate change.

We’re grateful to Samuel Pleeck and Mohammed Swalisu for analytical contributions to this article. We’re also grateful for comments from Anita Kappeli and Maya Verber. All views and any errors remain the responsibility of the authors.

[1] Several external aspects of the EU Green Deal have been criticized for introducing new non-tariff barriers – including in agricultural goods. Some critics argue that the EU's approach to climate cooperation amounts to “regulatory imperialism”, as opposed to an investment and cooperation-based approach, which strains their economies without providing adequate support for their climate-resilient and sustainable development.

[2] Global net zero at 1.5 degrees centigrade is roughly consistent with emissions of around 0.7 tonne per head globally in 2050 and many developing countries are currently below this.

[3] In scenarios looking at ‘fair shares’ of global finance for climate damage, all low income countries and lower middle income countries would be responsible for 1.8 per cent or less.

[4] These figures relate to the 75 per cent of CBAM revenues expected to be retained by the Commission with the remaining 25per cent going to Member States.

[5] Over the medium term, CBAM would likely raise much greater revenue, perhaps $80bn (€73bn) by 2040, as the carbon price it uses catches up with the EU’s carbon price which is also expected to increase over time.

[6] Based on figures from the European Parliament factsheet which suggest that the new package of resources amounting to some EUR 36 billion in 2028 is expected to correspond to 18-20% of the EU’s total revenues.

[7] This is before repayments declining gradually to EUR 14 bn towards the end of the repayment period in 2058, see also projections by Bruegel (2023).

[8] Maximising the Impact of EU Climate Finance https://www.cgdev.org/publication/maximising-impact-eu-climate-finance

[9] See Article 30, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023R0956

[10] Political Guidelines for the Next European Commission 2024−2029 https://commission.europa.eu/document/download/e6cd4328-673c-4e7a-8683-f63ffb2cf648_en?filename=Political%20Guidelines%202024-2029_EN.pdf#page=28

Topics

CITATION

Mitchell, Ian, and Beata Cichocka. 2024. Transforming EU Climate Leadership through CBAM Reform . Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: Daniel / Adobe Stock

{kind=link}