Recommended

Blog Post

Making IDA21 Work for Africa

Blog Post

Is Sub-Saharan Africa’s Credit Crunch Really Over?

Many low-income countries (LICs), particularly in sub-Saharan Africa, face the challenge of repaying loans in foreign currencies. With most of their debt in dollars or euros, these nations are in a difficult position: when their currency weakens, their debt burden goes up. This phenomenon—relying on foreign currencies for borrowing—is known as “original sin” and carries significant financial risk. In a recent paper, AfriCatalyst explores how local currency loans from the World Bank’s International Development Association (IDA) could help mitigate this risk.

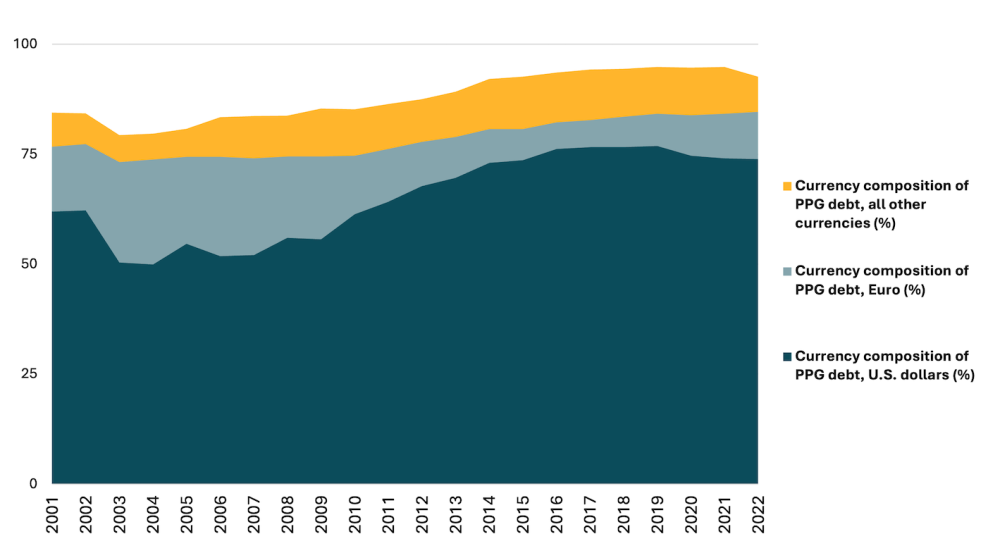

Figure 1. Currency composition of external long-term public and publicly-guaranteed debt (PPG)

Sub-Saharan Africa (excluding high-income)

Source: World Bank International Debt Statistics (IDS)

The debt trap of “original sin”

For years, LICs have borrowed in foreign currencies because it is often the only option available from external sources (e.g., development banks and private markets). And LICs often prefer hard currency borrowing—borrowing in a globally traded currency like dollars or euros—because it supports the buildup of reserves.

Global lenders also prefer stable options like the dollar or euro over riskier local currencies which can fluctuate wildly and may not be convertible. This dependence leaves LICs vulnerable to currency swings: every time their currency weakens against the dollar or other hard currencies, their debt effectively becomes more costly, adding to their financial burdens and complicating debt repayment.

Ethiopia is a clear example. With nearly 50 percent of its debt denominated in dollars, the value of its debts ballooned when its currency, the birr, depreciated. Between 2020 and 2022, the depreciation of the birr increased Ethiopia’s debt load by 18 percent, despite international efforts to provide relief.

Local currency lending

Local currency loans from multilateral development banks (MDBs) could ease debt volatility for low-income countries. By letting countries borrow in their own currency, MDBs could help ensure that loan repayments are more predictable, avoiding unexpected spikes in debt.

Although MDBs support local currency borrowing, these offerings have focused on private sector projects; sovereign loans (i.e., those to governments) are still largely offered in hard currency. Expanding local currency lending to sovereign loans could significantly improve debt sustainability for LICs. They would likely cost borrowers more, as MDBs do not want to assume currency risk, but would help shield LICs from the financial strain that currency depreciation often brings. Ultimately, the choice should be with borrowers.

Why IDA Is the best fit for local currency loans

IDA, the arm of the World Bank that provides concessional finance to lower-income countries, is uniquely positioned to lead this shift for four main reasons:

-

Focus on low-income borrowers: IDA lends to the poorest nations, especially in sub-Saharan Africa, which are the ones most vulnerable to currency risk. These countries could benefit significantly from stable, predictable debt repayments.

-

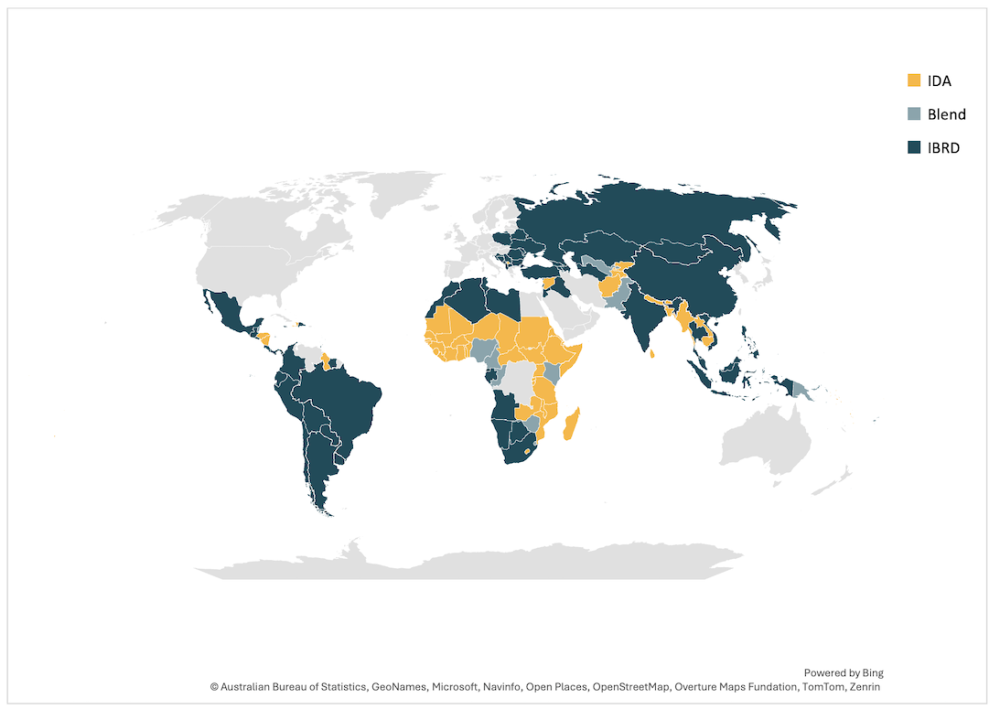

Figure 2. World Bank country classification by lending category

Source: World Bank Data Bank

-

-

Strong capacity-building programs: IDA already has programs to help countries improve their financial systems and debt management. These programs could provide a welcome opportunity to raise awareness of LIC debt management offices about the benefits of local currency finance, including FX risk mitigation options to boost demand for local currency loans.

-

Flexible funding model: Unlike private lenders that raise capital on international markets, IDA receives funding from member countries, which means it does not rely entirely on hard currency. This model could allow it to provide loans in local currencies more flexibly.

-

Cost of loans: The cost of IDA local currency loans could be cheaper than IDA credits with low interest rates if recipient countries regularly experience significant drops in local currency value.

Addressing risks and challenges

Local currency lending is not without challenges. Because IDA loan tenures are so long—fifty years and likely increasing to sixty after the next IDA replenishment—local currency lending poses very high risks. If IDA agreed to offer loans denominated in local currency, it would want to mitigate risks associated with currency depreciations. This means that IDA would charge a premium intended to hedge against that risk, which could discourage uptake. There may be strategies to enable IDA to offer local currency loans without demanding a significant premium, such as seeking donor-backed foreign exchange (FX) risk guarantees.

Another concern is ‘moral hazard’: since currency devaluation would reduce the real value of repayments, local currency lending would create a disincentive toward good economic management. To address this risk, IDA could lend in both local and foreign currencies to maintain stability and sustainability. Furthermore, a reasonable premium on local currency loans could help balance demand between foreign-denominated and local currency loans, discouraging excessive risk-taking.

Policy recommendations: A path forward for IDA

To make local currency lending a practical reality, the AfriCatalyst paper outlines several policy recommendations for IDA:

-

Capital market development (long term): Developing robust and well-regulated domestic capital markets is essential for sustainable local currency financing. IDA and other MDBs could do more to help LICs lay the groundwork for stronger capital markets by supporting regular local bond issuances, investing in government funds (including green bonds), and assisting with regulatory improvements.

-

Sovereign debt management (short to medium term): Improving sovereign debt management is critical. IDA could help LICs explore local currency options by raising awareness about hedged loans and filling knowledge gaps within debt management teams. Through training, technical assistance, and peer learning, IDA can help policymakers adopt effective debt management practices. Continued efforts to manage debt levels, including restructuring loans, could also help foster economic recovery and reduce long-term risks.

-

Local currency indexed loans (immediate term): IDA could start offering local currency loans to LICs, using one of the following options:

-

For countries with currencies pegged to major hard currencies like the US dollar or the euro, IDA could provide a higher proportion of foreign currency loans in their overall portfolio, given the ease of convertibility.

-

IDA could allow countries without fully convertible currencies to repay foreign currency loans in foreign currency at the prevailing exchange rate at the loan’s due date. The hard currency portion of these loans would include a grant to hedge currency risk—an approach currently under review by the Green Climate Fund.

-

Where a grant element is not feasible, IDA could offer a portion of the lending portfolio as synthetic local currency financing in partnership with TCX, a global currency exchange fund. A typical transaction would see IDA disburse the hard currency equivalent of the local currency loan amount using the prevailing exchange rate. The borrowing country would also make interest and principal repayments denominated in the same lending currency, but these payments would be indexed to a local currency interest and exchange rate determined at the time of the loan agreement. A swap transaction with TCX would hedge the interest rate and currency risk exposure created, ensuring that IDA always receives the planned hard currency amount.

-

A step toward more sustainable development finance

Transitioning to local currency lending could make debt more manageable for the world’s poorest countries. By addressing the issue of currency mismatch, IDA would not only ease debt burdens but also promote long-term stability and development. As other MDBs adopt similar approaches, this could lead to a much-needed transformation in development finance for low-income nations. While local currency options would be more costly to borrowers, it is important that the choice is ultimately with governments.

In a world where currency volatility often translates to fiscal stress, local currency loans can offer a practical, forward-looking solution. By taking the lead, IDA could give low-income countries a real opportunity for sustainable, resilient economic growth.

Read the full paper and learn more here.

AfriCatalyst is grateful to the Center for Global Development for its financial contribution to this research.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.

Thumbnail image by: malajscy / Adobe Stock