This is the sixth in a series of blogs looking at regional aspects of future global demographic and migration patterns discussed in my paper Global Mobility: Confronting A World Workforce Imbalance. You can read other blogs in the series here.

Gulf countries are world leaders in using worker mobility to fill employment gaps, a history that may serve them well as their populations age along with the rest of the planet and competition for immigrants intensifies. That said, the traditional model of immigration into much of the region has been temporary, and has involved considerable restrictions on the rights and opportunities of the migrants. Some Gulf countries are recognizing the need for change towards models that give migrants more autonomy, a necessary and welcome development.

In common with countries worldwide, those in the Gulf region are seeing falling fertility and aging populations. In common with most upper-middle-income and high-income economies, for some countries in the Gulf this has reached a stage where it implies a stagnating working age population and climbing old-age dependency ratios.

Under the United Nations medium forecast, the number of working age people in Saudi Arabia will be about 20 percent higher in 2050 than today, but the UAE will have fewer working age people in 2050 than 2020 (in Figure 1, the gray bars depict the percentage change forecast for the population aged 20-64 between 2020 and 2050). Meanwhile, the population aged 65 or older expressed as a percentage of the population 20-64 will climb from 5 percent to 28 percent in Saudi Arabia between 2020 and 2050. The same numbers for the UAE are 2 percent to 25 percent (in Figure 2, the teal bars show the change in predicted old-age dependency ratios 2020-2050). In order to keep total dependency ratios the same in 2020 as 2050, Saudi Arabia would need 21 percent more working age people than predicted in 2050 and the UAE more than twice the number predicted (the teal bars in the first figure depict the scale of this “worker gap”).

Figure 1. 2020-2050 working age population decline and 2050 worker gap

That said, these figures on the future “worker gap” reflect less a coming crisis in dependency for the region and far more very low current dependency ratios driven by migration patterns. Those same patterns also suggest countries in the region will remain outliers in terms of low dependency in 2050. Saudi Arabia was home to 13 million migrants in 2019 (this compared to a total population of 35 million), and the UAE 8.6 million (compared, stunningly, to a total population of 9.9 million).

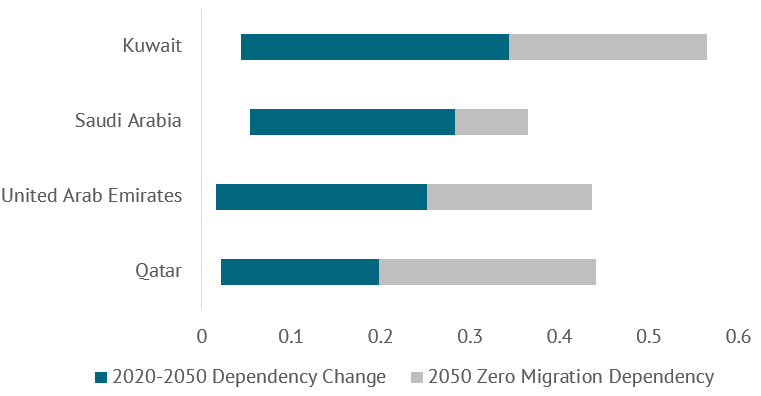

Large scale migration is predicted to continue by UN population experts, and that will help reduce future dependency ratios compared to a zero-migration forecast by more than 8 percent in Saudi Arabia and even greater amounts elsewhere in the region. Indeed, the top four economies worldwide in terms of reducing their old-age dependency ratio from the zero-migration scenario in 2050 thanks to predicted business-as-usual migration patterns are Qatar (24 percentage points), Kuwait (22 percent), Bahrain (20 percent), and the UAE (18 percent). (The gray bars in the second figure depict how much larger the 2050 dependency ratio is under the UN zero migration forecast.) Compare business-as-usual old-age dependency ratios in 2050 of between 20 and 35 percent in the Gulf countries in the figure to the forecast 78 percent in Spain, 74 percent in Italy, 58 percent in Germany, or 80 percent in Japan. And thanks to both the scale of migrant involvement in the economy and the sharp focus on temporary migration, Saudi Arabia is in the perhaps unique situation worldwide of seeing business-as-usual migration patterns to 2050 predicted to increase the (absolute) working age population more than the total population.

But there are questions as to whether the Gulf migration model is a good one for migrants or sustainable for the region. Survey evidence of Indian migrants to Gulf countries suggest migrants raise their income fivefold and appear aware of (and prepared to accept) the living and working conditions they will face on arrival. And in global Gallup surveys of migrant satisfaction, similar numbers of migrants in the Gulf Cooperation Council countries say they are thriving, as do migrants in the European Union. The proportion who want to stay where they are is similar across the two regions. Nonetheless, there are significant human rights concerns with many existing temporary worker programs in the region, and because of their working and living conditions, migrants suffered high rates of COVID-19 infections over the past 18 months. Rising global competition for migrants as rich countries age and poor countries get richer suggests that conditions should improve not only on moral grounds but because of both efficacy and necessity.

COVID-19 also suggested that temporary migration schemes can leave countries exposed in the face of restrictions on international travel. 151,990 workers permanently left Kuwait in 2020, and in April 2021, 350,000 workers were stuck abroad despite valid residency, leaving the country desperately short of workers. Models where residents stay long term or permanently may be more robust to temporary economic or mobility shocks.

The region has seen some movement towards reform. In 2020, Saudi Arabia announced it would give foreign workers the right to change jobs by transferring their sponsorship from one employer to another, as well as leave and re-enter the country and secure final exit visas without the consent of their employer. Qatar has introduced similar reforms. Of course, local populations and migrants alike face considerable rights abuses in many Gulf countries, suggesting a broader problem in attracting more people to the region as competition for migrants intensifies. If this is a spur to improved liberties for all in the Gulf, that would be another silver lining of the global workforce imbalance.

{kind=link}

{kind=link}