Recommended

Blog Post

The G20’s Climate Plans Don’t Do Enough to Limit Climate Debt

Blog Post

For Richer Countries, Climate Mitigation Should Begin at Home

One of the greater war crimes of the second half of the twentieth century was the massive and indiscriminate bombing of Indochina by the United States in the 1960s. The aerial campaign dropped more bombs than were used in the entirety of World War II. In North Vietnam, Operation Rolling Thunder destroyed more than half of the bridges and nearly 60 percent of the power plants alongside schools and houses, and killed at least tens of thousands of people. In 2011, Ted Miguel and Gerard Roland went looking for evidence of the long-term economic impact of the devastation. But they could “find no robust adverse impacts of US bombing on poverty rates, consumption levels, electricity infrastructure, literacy, or population density through 2002.” It was as if the mass destruction and loss of innocent life had never happened.

It would take an obscene amorality to suggest “well then, it didn’t matter.”

I think those who look at long-run economic forecasts of the impact of climate change and ask: “how can they be so small?” or look at those impacts and argue “see, it doesn’t matter” might be falling into a related error. It is true the long-term aggregate GDP impact of climate change might look underwhelming in much of the economics literature. In a way that should come as little surprise, in that the long-term aggregate impact of past disasters often looks pretty small in the literature too. But that doesn’t mean climate change is a small problem any more than those past disasters were; it means that long-term global GDP trends probably miss a large part of a big problem. “Lukewarmers” who use long-term global GDP forecasts to downplay the urgency of climate change are considerably too sanguine, then. But “doomsayers” who see the whole world heading toward a future amounting to a hotter version of the stone age are also wrong. The economic impact of climate change will vary considerably by country, with much of the effect driven by shorter-term shocks. And misdiagnosing the climate problem—either as small or universally existential—matters: it drives poor choices in the global policy response. The upcoming climate conference in Sharm El Sheikh is an opportunity to fix that.

Many very bad things are hard to see in long-term income data…

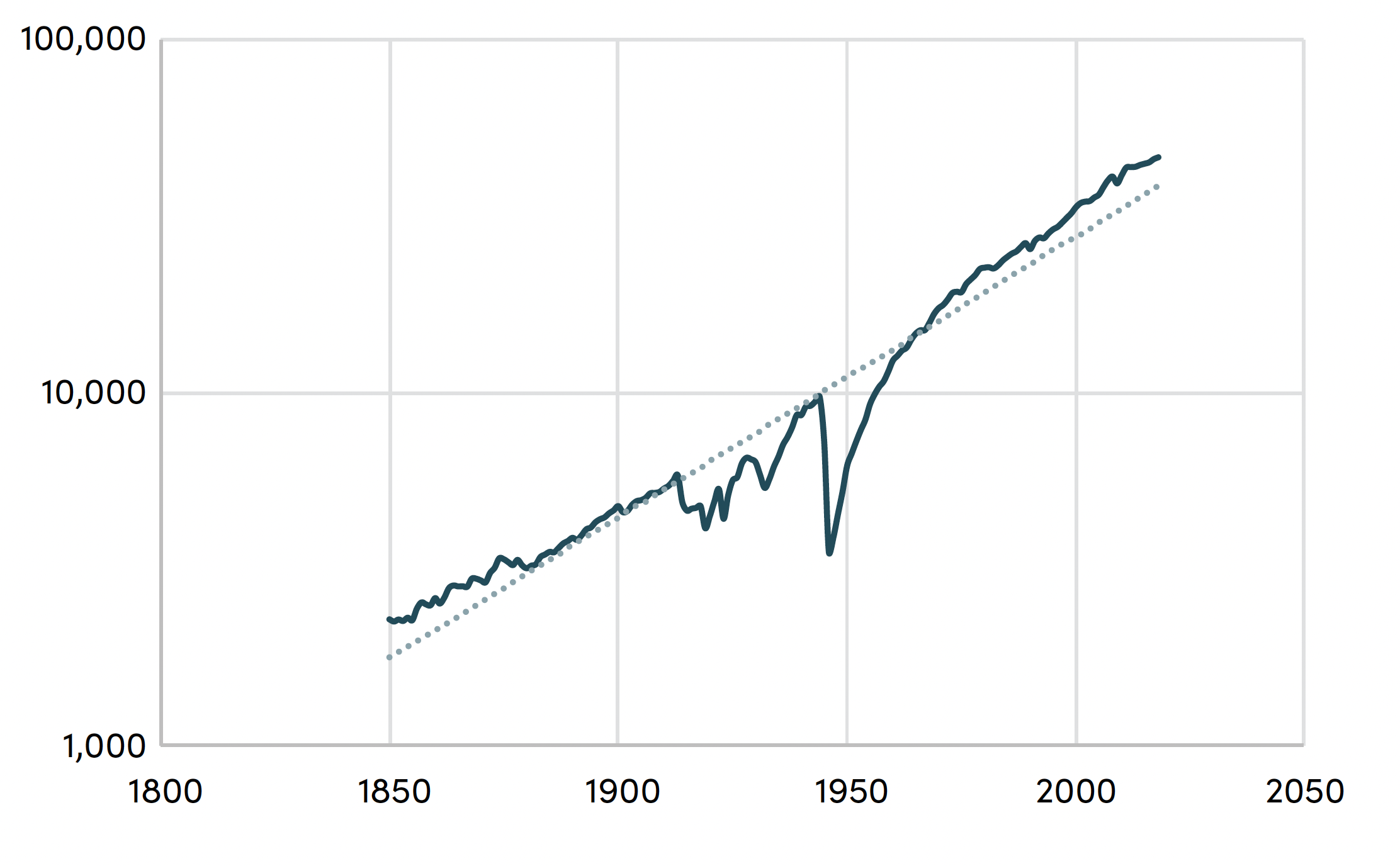

Amongst other economic shocks that apparently didn’t persist are the world wars. Organski and Kugler suggest the economic effects in Europe of the two world wars dissipated after 15–20 years, after which there was a return to prewar growth trends (although related work finds a longer-term impact of civil wars in poorer countries). Below is a graph of German GDP per capita over the long term—you can see both world wars and the Great Depression, but you can also see recovery to trend after that.

German GDP per capita, 1850-2022 (US$ PPP)

Some have gone so far as to argue natural disasters in particular might promote long-run growth. A number of studies suggest short-term but not sustained impacts of weather shocks, others find no long-term impact of disasters at all, and a meta-analysis that does conclude there is a negative impact suggested by the literature as a whole, especially in poorer countries, also notes there may be a serious problem of publication bias in that literature.

Long-term growth isn’t fundamentally about physical stuff that can be bombed, flooded, or turned into deserts; it is about ideas, technologies, and institutions, and the people who make them. Yet, that statistical studies are so inconclusive on the sustained impact of war, floods, fires, and earthquakes on aggregate GDP over decades does not mean the Four Horsemen of the Apocalypse have been given a bad rap—it means we are using a poor measure of the scale of the suffering they cause. The immorality of bombing people, for example, is not that it might affect their future income, but that the bombing itself is bad. It’s the wrong measuring stick.

…Including climate change…

Looking at climate change in particular, the IPCC’s AR5 synthesis report suggested “incomplete estimates of global annual economic losses for temperature increases of ~2.5°C above pre-industrial levels are between 0.2 and 2.0% of income (medium evidence, medium agreement). Losses are more likely than not to be greater, rather than smaller, than this range (limited evidence, high agreement).” By AR6 the IPCC was suggesting “under high warming (>4°C) and limited adaptation, the magnitude of decline in annual global GDP in 2100 relative to a non-global-warming scenario could exceed economic losses during the Great Recession in 2008–2009 and the COVID-19 pandemic in 2020.” (World GDP fell from $62.9 trillion to $62.1 trillion 2008 to 2009, and $84.7 trillion to $81.9 trillion 2019 to 2020, these are one-year declines, and the IPCC is suggesting climate change might cause the same impact over 90 years).

The IPCC’s estimates are toward the low end. A recent review of the literature using estimates of the impact of past temperature changes (alone) to forecast future impacts suggests global GDP will be 1-3 percent lower than otherwise in 2100 due to the impact of climate change (with a 95 percent confidence interval of -8.5 percent to +1.8 percent) consistent with most integrated assessment models, although some of those models suggest an impact up to 10 percent in the presence of extreme events like the collapse of the Greenland Ice Shelf. IMF staff suggests in the absence of mitigation policies, world real GDP per capita will be 7 percent lower than absent climate change by 2100, while abiding by the Paris Agreement would reduce the loss to about 1 percent. Burke et al. provide perhaps the largest estimate: a potential reduction of 23 percent from the global income that could be expected in 2100 absent climate change.

But even with Burke et al.’s approach, the annual global growth rate under their baseline scenario is 3.1 percent. Absent climate change, the global economy would be about 15.6 times larger in 2100 than 2010. They suggest the impact of climate change might be to bring that down to about 12 times larger. (They do suggest the potential growth impact could be as large as 50 percent under a scenario of very high emissions and very low baseline growth. In that case, the world economy would only be about seven times larger.) There is an immense amount of uncertainty about these estimates, to be sure, but that different approaches all come up with numbers that suggest, at worse, significantly slower global growth should provide some limited confidence in the idea that climate change is not likely to make the world poorer than it is, even though it will make it poorer than it might have been.

…That doesn’t mean they aren’t very bad things

In the long run in terms of aggregate global GDP per capita, the picture may be less dire than many expect—but we all know what Keynes said about the long run. Climate change is bad because farmers will lose their livelihoods, storm and wildfire victims will lose their houses and possessions. It will increase the intensity and frequency of events like the recent Pakistan floods. Even if (thankfully) the trend is strongly towards fewer people dying in natural disasters, and even if human resilience will mean those survivors rebuild lives, communities, and livelihoods elsewhere, more and more people will see their lives turned upside down. (To say nothing of the considerable impacts that don't appear in GDP forecasts, including on biodiversity). Simplistic assertions that end-of-century global impacts don’t justify a large and rapid response to the threat posed by climate change suggest the misery of billions over that period doesn’t count for much, because much of it will eventually end.

Climate impacts will be biggest in places least able to handle them…

Again, aggregate measures that hide local impacts are incredibly misleading on welfare effects: a huge majority of economists would agree that the welfare impact of a 50-percent income decline affecting just one in ten of the population is far larger than a welfare impact of a 5-percent income decline affecting everyone. And projected climate impacts—in terms of both volatility and growth—are worse where people can least afford them (and amongst those who contributed least to the warming trends in the first place). Pretis et al. project country levels of GDP per capita by the end of the century that are a median of 13 percent lower under 2 degrees warming than absent climate change. Poorer countries concentrated in the tropics see considerably larger losses. Burke et al. suggest under their worst scenario that some of the world’s poorest countries might actually be poorer in 2100 than today. (A related literature suggests looking at the national level misses hugely unequal impacts within them.) Hsiang et al. suggest a considerable and lasting impact of cyclones on growth, an impact once again concentrated in a minority of the world’s countries (and in parts of countries). Caribbean islands face income losses from larger, stronger cyclones due to climate change that generally exceed 20 percent of current GDP in net present value terms according to Hsiang et. al.’s analysis, while the United States might lose the equivalent of 5.9 percent of current GDP.

Simplistic assertions that climate change is an equally universal and long-term crisis for us all are wrong, too, then: some countries will suffer far more (and faster) than others. And that the assertions are wrong matters. Just as much as a false sense of security from small, long-term global GDP effects, the end-of-century armageddonism distracts from the fact that weather events are being made more extreme today, and that the effects of climate change are already unequally distributed.

…And that really matters for policy response

While lukewarmers argue for limiting any sort of policy response to climate, armageddonism leads to the wrong type of response. Not least, it pushes for immediate greenhouse gas emissions cuts over every other priority (including economic growth) everywhere, and encourages contemptible efforts to put an unfair burden of those emissions reductions on poorer countries under the painfully unaware statement “Mother Nature doesn’t care where the emissions have come from.” (Mother Nature may not, but the people you are lecturing surely do). The poor countries where climate change will have the biggest impact on weather, which are most reliant on agriculture, but also least able to self -insure against disasters, are also countries that are and will for decades be pretty much irrelevant to the climate mitigation battle.

So, what is the right policy direction? For richer countries, including upper-middle-income countries, that account for the bulk of global emissions and face less risk of catastrophic climate effects, mitigation should be a domestic priority—including research and development of technologies that make a low-carbon economy affordable worldwide. For poorer countries, that volatility and long-term GDP impacts are both likely to be larger threats suggests the need to focus on insurance and growth. They need (and climate justice calls for) rapid payout mechanisms to dampen the short-term impact of disasters and long-term economic support. But current global financing mechanisms are robbing them of both.

Global recovery funding comes slow and larded with unpleasant conditionality even when it is in response to factors completely out of recipient control (see the recent pandemic, food, and energy crises: remarkably few poorer countries are reaching out to the IMF for support because conditions are so unattractive). And a future disaster insurance mechanism can’t look anything like the small, expensive, and failed World Bank pandemic bonds program. Again, the financing poorer countries could use to support growth toward adaptation is wrapped up in red tape and being diverted to mitigation projects of dubious value in richer countries. It is an absolute travesty to take the existing (paltry) funding to back growth in poor countries most at risk to fund mitigation in richer larger countries more able to self-insure, and less at risk in the first place. In short, we may need an IMF for climate—but it can’t operate anything like the current IMF or World Bank when it comes to supporting those most at risk.

Climate change is a worldwide and potentially centuries-long event, but it is precipitating thousands of local and short-term crises that demand response. That means it is urgent to move away from thinking about climate change as “distant and unimportant” or “distant and universally existential” towards “immediate and differentiated.”

Related to that, I hope that the upcoming COP27 climate meetings in Egypt make a clear set of statements that:

-

The volatility and growth impacts of climate change are concentrated in countries least able to bear them and which carry very little responsibility for creating the climate problem in the first place.

-

Economic growth is the most powerful tool to support adaptation, and should be the priority for those countries.

-

The international community, and especially richer countries responsible for the great bulk of emissions, should support that growth alongside effective crisis-response mechanisms to reduce the short-term impact of natural disasters linked to climate.

-

This will take reform of the international financial architecture to ensure greater funding for development focused on the poorest countries and large-scale, affordable, rapid, and conditionality-free emergency financing mechanisms for all developing countries at high risk.

-

Richer countries (including upper-middle-income countries) should take the lead on domestic mitigation efforts including technology development, and be far more aggressive in their commitments to reduce emissions.

Climate justice calls for nothing less.

Topics

CITATION

Kenny, Charles. 2022. Climate Change May Have Only Small Effects on Long-Run Global GDP. So What?. Center for Global Development.DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.