Recommended

Blog Post

Will the US-Africa Leaders Summit Reorient Africa Policy?

POLICY PAPER

Greening the US Sovereign Bond Guarantee Program

More from the series

Blog Post

How Does MCC Fit Into the New US Commitment to Africa?

Blog Post

Biden’s Visa Breakdown

This blog is one in a series by experts across the Center for Global Development ahead of the 2022 US-Africa Leaders Summit. These posts aim to re-examine US-Africa policy and put forward recommendations to deliver on a more resilient, deeper, and mutually beneficial partnership between the United States and the nations of Africa.

If the Biden administration wants to forge stronger bonds with African governments in the lead up to mid-December’s US-Africa Leaders Summit, it will have to focus on meeting the needs of those governments during a particularly difficult period. Multiple economic shocks have severely limited the borrowing capacity and fiscal space of lower-income countries, including many on the African continent. Yet, direct measures of support for developing country governments are almost entirely absent from the US government’s current toolkit. Instead, US policy has focused on delivering traditional foreign aid and humanitarian support offered through non-government channels, alongside a nascent global infrastructure initiative that relies on private sector investment.

While these measures undoubtedly hold some appeal, African leaders would very likely prefer more direct measures of support at a time when their budgets are under significant stress. One useful but greatly underutilized instrument of support is the US guarantee on foreign governments’ external borrowing. Sovereign loan guarantees have been offered by the US government in a small number of countries, driven by foreign policy objectives. Israel has the been the primary beneficiary, but guarantees have also been deployed for Ukraine’s government in the past decade, as well as the newly democratic governments in North Africa during the Arab Spring.

An urgent need for new financing

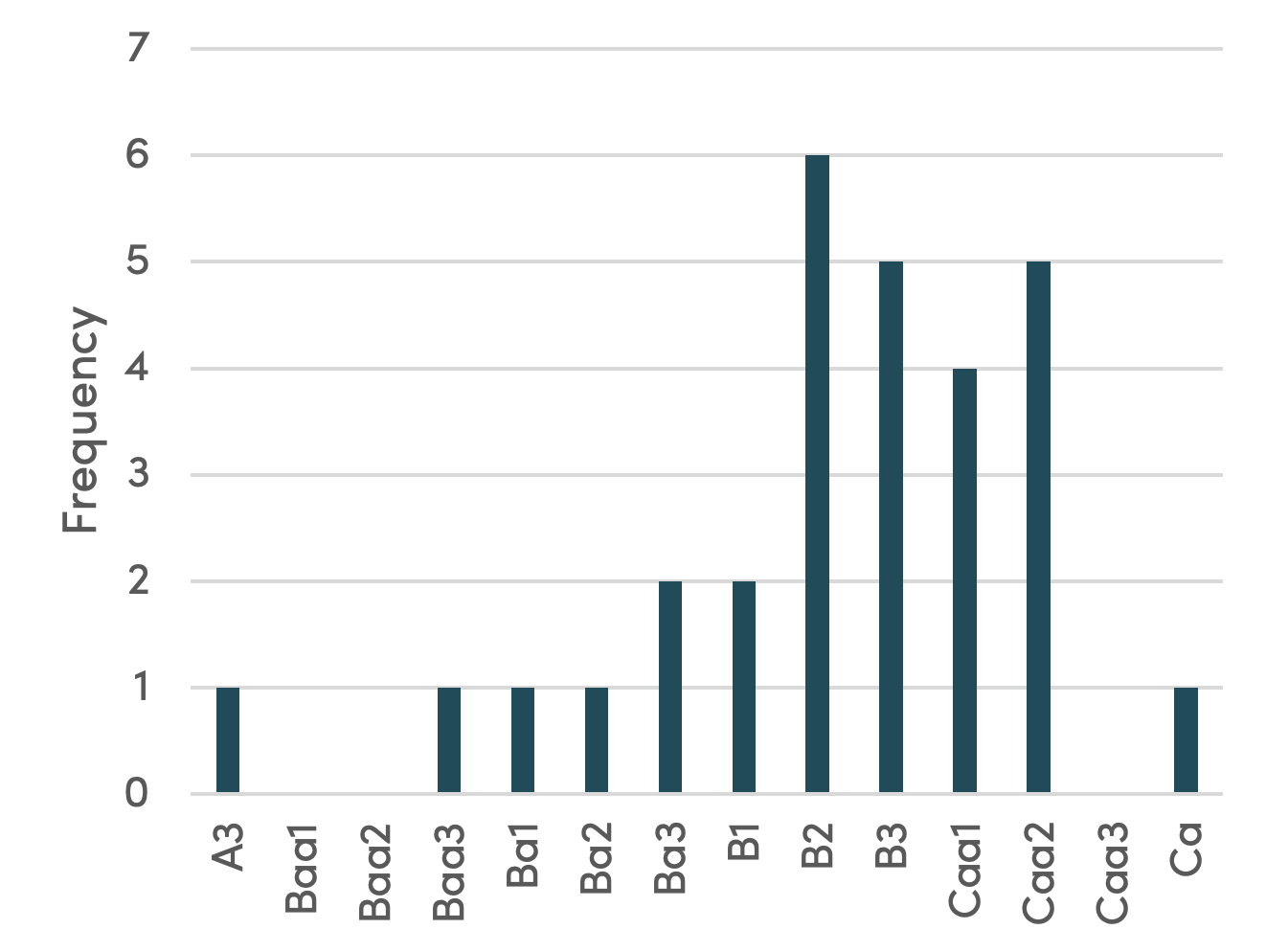

Just how bad is the problem facing African governments today? Under the best of circumstances, countries on the higher end of Africa’s credit ratings distribution pay interest rates hundreds of basis points higher than the US Treasury rate on their sovereign borrowings. For those on lower end of Africa’s credit ratings distribution, borrowing costs can easily be double, triple, or quadruple those of wealthy countries.

Figure 1. Few African countries currently hold Moody’s credit ratings above the Baa3 threshold for “investment grade” bonds

Source: Bloomberg Data, extracted Nov. 15, 2022

As credit markets tighten, the disparity between rich and poor countries’ cost of borrowing grows. Figure 2, which depicts the yield to maturity of Egyptian, Moroccan, and US medium-term bonds (all due in Q3/Q4 2027) highlights this trend. Between November 2021 and 2022, the yield of the Aaa-rated US Treasury bond increased by 252 basis points. Over the same period, Morocco’s Ba1-rated bond yields increased by 317 basis points and Egypt’s B2-rated bond yields increased by 525 basis points. When credit conditions tighten, countries on the lower end of the credit ratings distribution feel the effects most acutely. And to the extent that the yields below reflect the interest rates investors would expect to earn on new lending to similarly rated sovereigns, it is easy to see how African governments could be priced out of (or forced into default by) commercial credit markets.

Figure 2. The gap between US and African yields has widened

Source: Bloomberg Data (ISINs = XS2391394348, XS2270576619, US91282CAY75), extracted Nov. 15, 2022

With a growing number of African governments facing much higher costs of borrowing or priced out of commercial markets altogether, there is a pressing need to identify other sources of external funding to meet financing needs, including service on existing debt. Many African governments—like Kenya—also face looming repayments of previous bond issuances. International financial institutions (IFIs) like the International Monetary Fund, World Bank, and African Development Bank play a key role during crisis periods, stepping in with concessional finance when commercial options grow scarce. And the United States has generally looked to these institutions rather than provide direct support.

But with the Biden administration’s prioritization of “great power competition” with China, alongside growing frustration with the scale and quality of the IFIs’ lending programs, there is an opportunity to rely more on bilateral financing options.

Enter the US sovereign loan guarantee

Sovereign loan guarantees (SLGs) put the full faith and credit of the US government behind a limited debt issuance by an emerging market sovereign borrower. The United States agrees to repay lenders should a borrower country default, effectively lending its credit rating (and therefore its cost of borrowing) to the borrower country. In return, the borrower country often agrees to make some commitments regarding financial transparency or other areas of policy like climate adaptation spending.

SLGs are a uniquely efficient form of foreign assistance because, unlike direct lending or project finance, they don’t require a large financial outlay on the part of the US government. When the US issues an SLG, federal accounting rules require that the implementing agency (historically USAID) sets aside funds to cover the “subsidy cost,” equal to the expected value of the guarantee’s contingent liability. Historically, this expected value has been a fraction of the total guarantee value, because it reflects the probability that the borrower country defaults on the guaranteed loan. In the history of the US SLG program, there has never been a default on a US SLG, so every dollar set aside as a subsidy cost has been returned to the US treasury upon successful repayment of the guaranteed loan.

SLGs would only be appropriate in a limited range of countries. Because an SLG’s subsidy rate—the proportion of the total guarantee that must be set aside as a subsidy cost—is a function of the borrower country’s credit rating, SLGs are only effective for countries within a certain range of credit ratings. If a country’s credit rating is too low, the cost of guaranteeing its debt may outweigh the borrowing cost reductions that the guarantee yields. Conversely, if a country’s credit rating is too high, guarantees become unnecessary because they fail provide substantial interest rate reductions. When it comes to Africa’s emerging market economies, however, many countries have credit scores “just right” for SLGs.

Figure 3. Many of Africa’s emerging market countries have credit scores “just right” for SLGs

Source: Moody’s credit ratings data from Bloomberg, SLG efficacy estimates from Greening the US Sovereign Bond Guarantee Program: A Proposal to Boost Climate-Directed Sovereign Finance in Developing Countries

For those “Goldilocks” countries that fall into the effective range for US SLGs, the potential benefits of the credit enhancement are large. Previous CGD analysis estimates that eleven historical SLGs on $9.2 billion in sovereign bond issuances saved borrower countries some $2.1 billion, or 23 percent of their borrowing costs. Moreover, there is evidence that credit enhancements like US SLGs have been instrumental in facilitating market access for countries that would otherwise struggle to access private capital. The total subsidy cost of the eleven historical US SLGs was $1.7 billion, so every dollar set aside as a subsidy cost leveraged $5.6 in new borrowings for developing countries. And since none of these countries defaulted on the guaranteed debt, the long-term cost to the US government of these eleven SLGs was negligible.

A political roadblock

Unfortunately, the SLG program is stuck in bureaucratic limbo. Absent a political-level embrace, the guarantees are viewed entirely as a liability by agency actors. The Better Utilization of Investments Leading to Development (BUILD) Act of 2018 authorized the transfer of the SLG program (with all its personnel and liabilities) from USAID to the newly created Development Finance Corporation (DFC). But in “authorizing” the transfer and not requiring it, BUILD gave DFC the authority to subsume USAID’s SLG infrastructure and expertise without assuming responsibility for running the actual SLG program.

Because of the necessity for congressional action to fund SLG subsidies, the implementing agency has very little scope to decide when and where SLGs are appropriate. SLG liabilities, by contrast, sit squarely on the books of the implementing agency. Moreover, SLGs—especially politically-motivated SLGs to countries already bordering on debt distress—can be extremely expensive to provision. Ukraine’s 2015 SLG on a $1 billion in bond issuance required that USAID set aside $446.5 million in subsidy costs. Congress has not appropriated any funds to DFC to specifically fund SLGs, so any SLGs issued by DFC would either require a specific subsidy appropriation or require DFC to fund the subsidy cost using its own program budget.. Completing the transfer of the SLG program to DFC as authorized by the BUILD Act could therefore be viewed as lose-lose scenario for the new agency, as it would constrain the agency’s operating budget and lending potential without giving DFC any agency to allocate new SLGs without external authorization.

The result is a bureaucratic morass. As of this writing, it remains unclear which government agency would oversee a loan guarantee if a new one was to be issued. Congress itself has asked for clarification on this issue by directing relevant department heads to submit a joint statement detailing the current liabilities of the SLG program, the impact of transferring the program to each of several relevant agencies, and the status of any ongoing program transfer.

For African governments in need of immediate budget support, this situation provides little comfort. The SLG program presents a uniquely powerful tool in the US development finance arsenal for supporting emerging market governments through a particularly difficult period. If used judiciously, SLGs could provide many African governments with the financial support they need to better confront the current array of crises and in turn strengthen their bonds with the United States. But time is of the essence. Breaking through the bureaucratic deadlock that has stalled the SLG program is a political imperative. The US-Africa Leaders Summit ought to provide the motivating force for the White House to act.

Stay tuned for more analysis on the summit in the coming days, and sign up for our US development policy newsletter to get updates in your inbox.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.