Late last year the IMF confronted two difficult but related policy challenges…

There were strenuous and mounting calls for the IMF to reduce or eliminate surcharges that raised interest costs for the IMF’s large borrowers. At the same time, the IMF’s Poverty Reduction and Growth Trust (PRGT) was fast approaching a financial cliff which could see its lending capacity collapse.

As explained in more detail in a CGD note, the successful resolution of both these challenges required some difficult tradeoffs. Most IMF shareholders were probably not happy with all aspects of the reforms to surcharges and the PRGT. But a compromise was forged and the broad support for the combined packages of reforms, despite the backdrop of widening geopolitical divisions, provides lessons for future reforms.

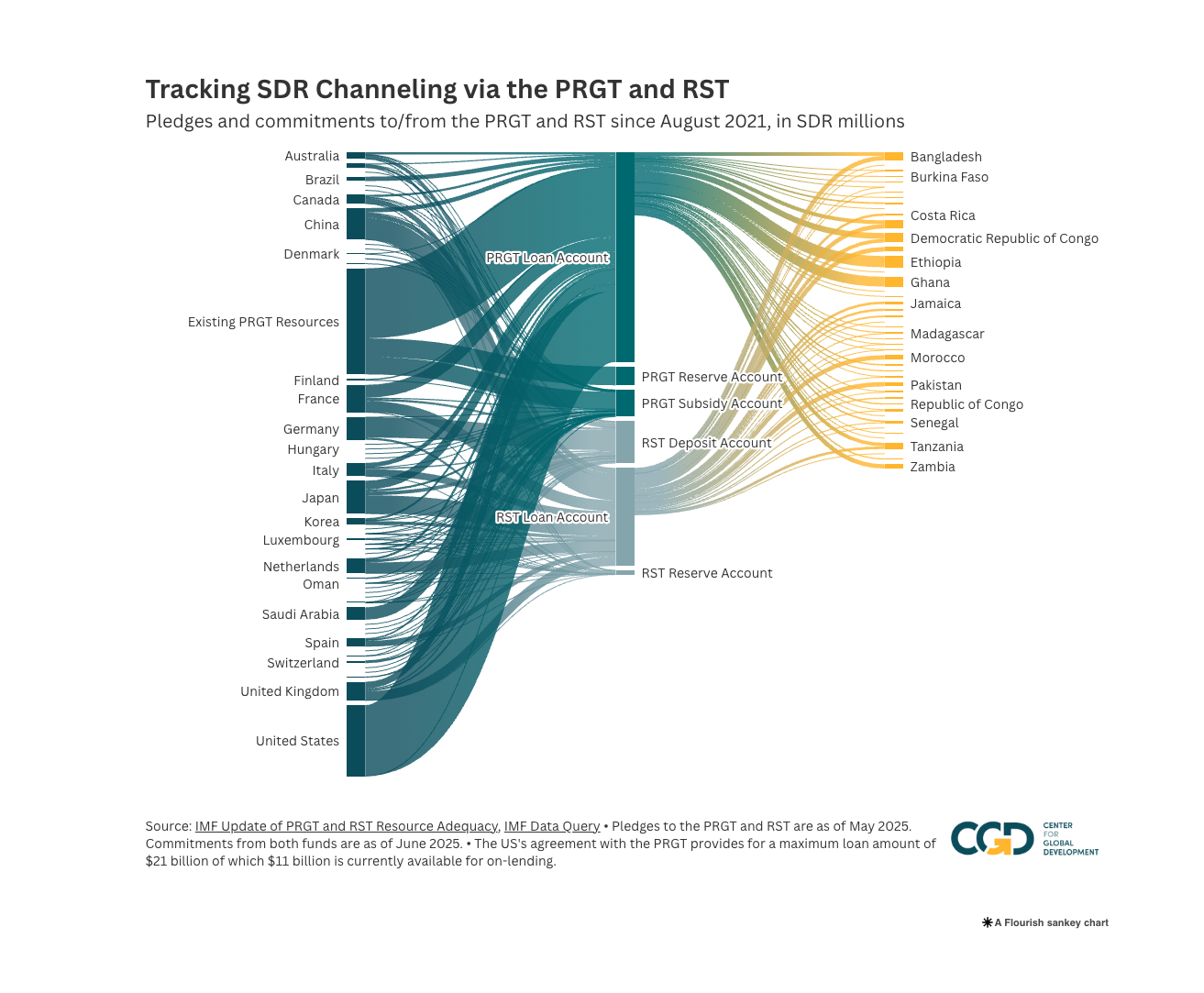

And while the deal is done in principle, it still requires commitment by 90 percent of the IMF’s membership to make the transfer of resources effective. So far only 25 percent has committed to the scheme. Outside vigilance will be important to get the PRGT the support in needs,

The PRGT urgently needed a large injection of new resources…

Since COVID, the lending capacity of the PRGT had been severely eroded. The subsidy resources that enable the PRGT to provide interest-free loans to 70 low-income countries (LICs) had been depleted by a fivefold increase in lending—from SDR 1 billion a year before the pandemic to over SDR 5 billion a year in 2020–24—and an almost equally sharp rise in the SDR interest rate. And if these resources were not replenished the PRGT’s long term lending capacity was projected to collapse to SDR 1 billion within two years, falling far short of LICs’ needs.

Raising the PRGT’s sustainable lending capacity is costly. The IMF estimated that without changes to the PRGT’s lending policies, an injection of over SDR 9 billion (or about $12 billion) in new subsidy resources would be needed to yield a long-term annual lending capacity of SDR 2.7 billion. And hard transfers, not loans, were needed to plug this gap.

Gold sales were not an option…

Selling just 5 percent of the IMF’s gold, which is held on the balance sheet at a fraction of its market value, could generate profits of well over SDR 10 billion. But this option was not on the table. Gold sales must be approved by a majority of at least 85 percent of the IMF’s membership and securing the necessary support from the US, which holds 17 percent of the voting power, would also have required backing from the US Congress.

Using some of the IMF’s reserves was the only feasible way forward...

The scale of the PRGT’s needs also ruled out reliance on donations from member countries. Instead of gold or large donations, the agreed strategy relies heavily on financing from the IMF’s reserves. These “precautionary balances,” in IMF terminology, held to mitigate risks on the balance sheet, had reached a long-standing target of SDR 25 billion early in 2024. And their projected path suggested ample scope—in the absence of policy changes—to use reserves generated over the next 5 years to support the PRGT without cutting into the SDR 25 billion target.

But the PRGT was not the only call on reserves…

Many countries wanted to reduce surcharges, which are additional interest the IMF levies on large (non-PRGT) borrowers. The clamor to cut or eliminate surcharges that were seen as placing an excessive burden on borrowers grew louder as the IMF’s basic lending rate that is linked to the SDR interest rate, rose in line with higher market rates. By September 2024, larger borrowers of the IMF’s non-concessional loans faced a marginal interest rate of about 7.5 percent, including surcharges of up to 3 percent.

As well as providing an incentive for borrowers to repay loans early, surcharges have for many years been a major driver of the IMF’s reserve accumulation. (By adding to lending income, they have bolstered the IMF’s total net income, allowing more to be added to reserves at the end of each fiscal year). And looking to the future, eliminating surcharges would have sharply lowered the path of reserve growth and not left enough reserves to plug the gaping hole in the PRGT’s finances. Conversely, using reserves to meet the bulk of the PRGT’s financing needs of over SDR 9 billion would have left little scope to cut surcharges while maintaining a reserve buffer of SDR 25 billion.

The resulting solution involved tradeoffs between competing objectives:

- The costs of borrowing from the IMF were lowered significantly but surcharges were not eliminated. Surcharges were adjusted so that fewer borrowers would pay them, and at a lower rate. In addition, the reforms also lowered the “basic rate of charge” that all non-concessional borrowers pay over the SDR interest rate. In this way, costs were reduced for all borrowers, not just those subject to surcharges. But surcharges will continue to provide an incentive to repay early and contribute to net income and reserves.

- The PRGT’s financing needs were reduced by targeting the PRGT’s zero interest rate on about 30 poorer LICs. The other 40 PRGT-eligible countries with higher incomes are now charged a subsidized interest rate of 40 percent or 70 percent of the prevailing SDR interest rate, with those having access to private capital markets paying the higher rate. Focusing scarce subsidy resources on the poorer LICS, who have also fared worse since COVID, was a better choice than reducing subsidies for all PRGT users.

- Most of the projected reserve accumulation in the next five years will be used to support the PRGT. Reserve growth will be slowed by the reductions in charges and surcharges, but this is still expected to allow the PRGT’s needs to be met while precautionary balances remain just above the target level of SDR 25 billion.

However, this long-term financing strategy for the PRGT still faces some risks…

- The IMF’s income and reserve position needs to remain strong enough for reserves to be used to support the PRGT. While the bulk of projected net income in the next five years is expected to be used to support the PRGT, the actual income position is subject to many uncertainties, including the vagaries of interest rates and loan demand. Adverse developments could also prompt a decision to build up greater reserves.

- The PRGT’s long term lending envelope of SDR 2.7 billion may not be adequate to meet the needs of LICs. In the early years, lending could exceed SDR 2.7 billion a year without seriously affecting future capacity. But a sustained higher level of demand which could, for example, arise from the severe cuts in development assistance seen after the financing strategy was approved, would need to be offset by additional financing or policy changes.

- Moving reserves to the PRGT in the next five years will require the overwhelming support of IMF’s membership.

- Under the IMF’s Articles of Agreement—its constitution—reserves cannot be simply transferred directly to the PRGT. Instead, they can be distributed to the membership pro-rata to quota shares and it would then be up to each member to agree to use their share to support the PRGT.

- To minimize possible “leakage,” it was agreed that before any reserve distributions take place, member governments accounting for at least 90 percent of the planned reserve distributions must commit to using their shares to support the PRGT

- The approved financial architecture provides a safeguard against possible prolonged delays in obtaining this level of assurances. Specifically, annual reserve distributions are to be placed in an interim IMF account pending attainment of adequate assurances for at least 90 percent to be moved to the PRGT. In the interim period, interest income earned by this account will be credited to the PRGT’s subsidy accounts. The sooner the threshold of 90 percent is reached, the sooner the financial security of the PRGT can be assured.

- The 90 percent threshold of assurances must ultimately be reached. If not, the funds in the interim account could after five years revert to reserves—leaving a gaping hole in the PRGT’s finances. And there is still a long way to go. The IMF reported that by March 2025, assurances totaled about 25 percent of the planned distribution.

- While the IMF staff is committed to getting to the 90 percent threshold, concerned observers outside the IMF need to be vigilant in getting every IMF member country to agree to the give their formal support.

The PRGT and surcharge reforms provide a model for future action…

The PRGT will be better placed to meet LICs’ needs and reducing surcharges that had long been a major concern for borrowers will help to bolster the legitimacy the organization. And despite an environment of geopolitical divisions—which also ruled out “easier” options like gold sales—compromises were found to engender the necessary broad support of the membership. It is crucial the IMF continues to demonstrate its value for the membership responding to their changing needs and concerns. As in the case of the reforms discussed here, this may well entail a focus on reforms that improve operations using only existing resources.