Recommended

This blog is one in a series by experts across the Center for Global Development ahead of the 2022 US-Africa Leaders Summit. These posts aim to re-examine US-Africa policy and put forward recommendations to deliver on a more resilient, deeper, and mutually beneficial partnership between the United States and the nations of Africa.

Debt and climate change are defining challenges for many countries in Africa. Governments across the continent are seeing their debt burdens mount—some to unsustainable levels—as they race to mobilize resources to adapt and respond to the increasingly severe climate crisis.

Debt-for-climate (D4C) swaps—a conditional form of debt relief based on a country’s commitment to undertake a series of investments in climate— are often cited as an elegant theoretical solution for these twin crises. But their implementation track record has not always lived up to their potential. A recent IMF report found that they have not always been successful in restoring debt sustainability or mobilizing additional climate financing. Experts have also raised questions around whether linking debt relief to climate or other green or social conditionality may even push countries into shallower restructurings than they would otherwise need. But D4Cs can still be useful instruments if they are deployed under the right circumstances. According to the IMF study, they are most effective in contexts where a country needs support reprofiling or restructuring a specific instrument, rather than for countries where a more systemic restructuring exercise is warranted to restore sustainability. And they must be designed so that the debt relief has material impact on the sovereign outlook and does not just kick larger debt sustainability issues down the road. Finally, they must mobilize investments above and beyond what a standard grant could have generated.

The US Development Finance Corporation (DFC) has already experimented with this type of transaction by guaranteeing the debt swap. We see a strong case for DFC to pilot a series of D4Cs across a sample of African countries, building off the lessons from the IMF report and its own experience with blue bonds in Belize and elsewhere. While the focus here is on climate, the swap program could also be adapted for health or other areas where donor and government spending priorities align. In the context of the upcoming 2022 US-Africa Leaders’ Summit, a scaled-up DFC debt-for-climate program could be an important US contribution to the continent’s economic and climate finance needs.

DFC’s record on climate and debt

DFC has placed a strategic emphasis on increasing climate finance, and the agency’s climate-linked investments have grown considerably over the past two years. It committed $2.3 billion for climate-linked projects in FY2022, a sizeable increase from FY2021, when it committed $454 million across 21 climate-linked transactions. DFC’s climate finance portfolio mostly focuses on mitigation and finance for clean energy, with most of its exposure concentrated in middle-income countries.

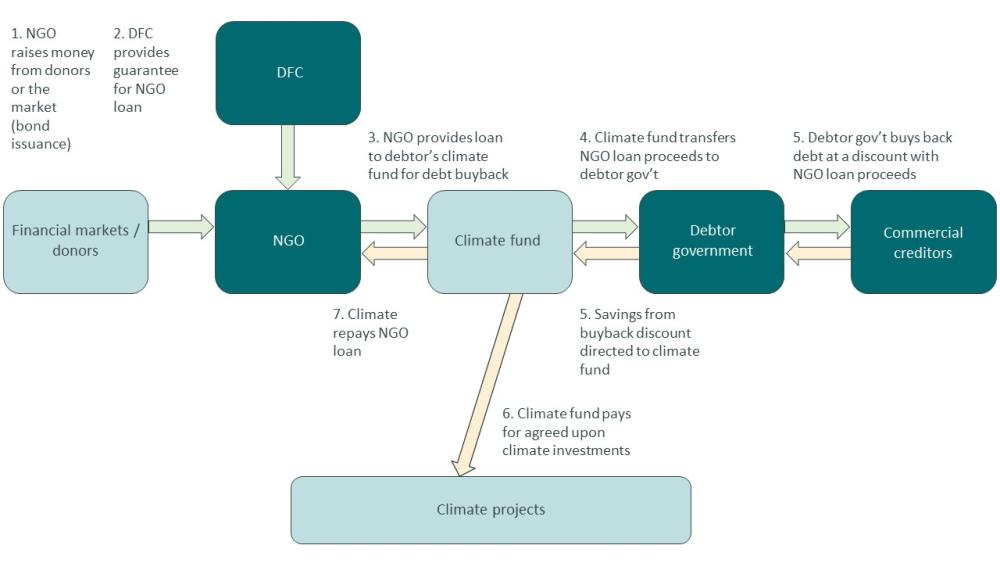

DFC has also supported debt swap-like projects in the form of “blue bonds” or blue loans, which have largely focused on private commercial debt. In partnership with The Nature Conservancy (TNC), DFC has made commitments to blue bond projects in Kenya, Belize, Saint Lucia, and Barbados. The general model is that TNC provides the country with a loan that is insured by DFC—which enables it to achieve investment grade and lower funding costs—to buy back a debt instrument at a discount. The country then uses the savings generated by this transaction to invest in marine conservation.

Figure 1. Illustrative example of a DFC debt swap transaction

The Belize project is DFC’s largest debt swap operation to date. It allowed Belize to reduce its external debt stock by 9 percentage points of GDP and gave the government space to mount an ambitious coastal conservation program. The blue bond raised $364 million, of which $310 was used to retire Belize’s outstanding $546 million bond and $24 million was put into a trust fund to protect its coral reefs. But the deal has also raised important questions, echoed in the IMF report, around whether these types of swap arrangements are appropriate for countries with deeper sustainability issues. Belize’s debt swap reduced its debt-to-GDP ratio from 108.3 to 99.5 percent. But, the IMF continues to assess the country’s debt as unsustainable in the absence of additional measures, raising important questions around whether a more comprehensive restructuring would have been more appropriate.

A proposal for a DFC debt-for-climate program in African countries

We see a strong case for a well-designed and targeted DFC D4C program across several countries in sub-Saharan Africa. DFC could develop partnerships with other foundations, NGOs, and international organizations to develop a D4C program. We also see a potential role for USAID both as a source of government co-financing and as a source of technical assistance.

These programs would have two core objectives: materially improving a country’s debt outlook and mobilizing additional financing for climate resilience. DFC would consult closely with the IMF to determine the implications of the transaction on the country’s long-term sustainability outlook. A key rule of thumb should be that relief provided should also be deep enough to ensure that the additional spending for climate is not at the expense of core government spending in the social sectors. Programs funded under this initiative could include conservation of important carbons sinks, and other natural capital investments both on the African coasts and across savannahs and forests.

We created a D4C “readiness” index to identify countries that would be good candidates for D4Cs based on some of the key criteria the IMF put forward and other factors including climate vulnerability, natural capital levels, and estimated grant availability (see the full workbook here).

On top of these considerations, we screened out countries with unsustainable debt outlooks and large creditor bases. This gives us a list of seven countries.

Table 1. Potential country partners

|

Country |

Income classification |

Debt-to-GDP (%) |

Carbon sink and conservation considerations |

Non-IFI debt owed to non-Paris Club and commercial creditors (%) |

Total public external debt ($ bn) |

|

Namibia |

UMIC |

70.3 |

Miombo woodlands |

- |

2.8 |

|

Angola |

LMIC |

86.3 |

Congo basin |

73 |

46.7 |

|

Gabon |

UMIC |

71.2 |

Congo basin |

84 |

6.3 |

|

Tanzania |

LMIC |

|

Coral reefs and blue economy |

65 |

18.9 |

|

Liberia |

LIC |

52.9 |

Tropical rainforests; marine conservation and blue economy |

100 |

1.0 |

|

Botswana |

UMIC |

|

|

77 |

1.5 |

|

Nigeria |

LMIC |

35.3 |

Potential emerging carbon economy, mitigation projects could have a large benefit |

95 |

34.3 |

Sources: World Bank International Debt Statistics, IMF, Climate Vulnerability Monitor, Natural Capital Index.

Governments should be put in the driver’s seat to define the specific spending and policy priorities to be undertaken in the context of the D4C. Ideally, a swap with DFC’s participation will build on a country’s existing policy agenda. DFC can also help ensure that its D4Cs promote economic benefits that extend beyond just climate considerations. For instance, the blue bonds programs contributed to the preservation of marine ecosystems, which are also important hubs for economic activity and livelihoods.

Debt-for-climate swaps are not new to the scene. But there is fresh interest in them as tools for today’s concurrent climate and debt crises. And alongside the political momentum, we have a fresh evidentiary base around what works and what does not. Building on new knowledge, DFC can capitalize on the demand—and its own experience—to increase its role in these transactions and shape them so they serve countries in need.

Topics

DISCLAIMER & PERMISSIONS

CGD's publications reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions. You may use and disseminate CGD's publications under these conditions.